Tyson Foods Inc. TSN -4.83% won the auction for Hillshire Brands Co. HSH +0.01% , but it ended up paying hundreds of millions of dollars more than necessary to beat the next-best offer.

Tyson Foods Inc. TSN -4.83% won the auction for Hillshire Brands Co. HSH +0.01% , but it ended up paying hundreds of millions of dollars more than necessary to beat the next-best offer.

That was due to the secretive way auctions for companies are conducted. The setup is not like a live art auction when a bidder knows where his rival stands. Rather, it is more like the frenzied sale of a house in a prime location, where a bidder tucks a price into an envelope, trying to guess what dollar figure it needs to come out on top.

Tyson’s price of $63 a share for the Chicago-based maker of Jimmy Dean sausages and other meat products, or $7.7 billion, turned out to be far more than Tyson needed to pay to beat out Pilgrim’s Pride Corp. PPC +1.75% , a unit of Brazilian meatpacking giant JBSSA, JBSS3.BR +1.90% to buy Hillshire.

Pilgrim’s Pride joined the weekend auction for Hillshire—but, as it turned out, the company stuck with its $55-a-share bid that it had made last week. The company confirmed that Monday, but Tyson didn’t know it during the auction, said a person familiar with Tyson’s offer. Under the rules of the bidding, Tyson could have won by exceeding the Pilgrim’s Pride bid by around $2.50 a share. Because Pilgrim’s Pride held firm at $55 a share, Tyson could have won with a bid of around $57.50, or $7.05 billion, said people familiar with the sale.

Want to publish your own articles on DistilINFO Publications?

Send us an email, we will get in touch with you.

On Monday, Tyson’s chief executive Donnie Smithdefended his deal, saying the combined company could cut about $300 million in annual costs and that the deal has the potential to increase Hillshire’s sales in schools and elsewhere. “We’re purchasing these assets not just for their value today, but for their potential over time,” Mr. Smith said.

Another person familiar with the deal said Tyson’s bidding approach was meant to knock Pilgrim’s Pride out of the contest.

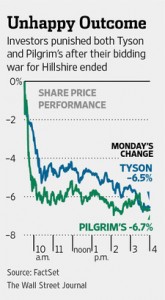

Shareholders of both companies were unhappy. The stock of Tyson closed down 6.5% to $37.50, while Pilgrim’s Pride shares fell 6.7% to $24.51.

Bill Lovette, Pilgrim’s chief executive officer said, “As a disciplined acquirer, we determined that it was in the best interests of our shareholders not to increase our proposed price of $55.00 per share in cash.”

The frenzy for Hillshire, a ping-pong match of four bids between two rivals in that many weeks, is the latest sign of the hot mergers and acquisitions market, in which some sellers have far more leverage than in recent years when deal activity was lackluster.

Monday marked a record day for deal premiums. Tyson agreed to pay around 70% more for Hillshire than the company’s stock market valuation before bidding for it began late last month. The premium it is paying is the second-highest this year for deals of $1 billion or more, according to Dealogic, which tracked the premiums on a one-week-before-bid-announcement basis. The highest is Merck MRK +0.19%& Co.’s $3.85 billion deal for Idenix Pharmaceuticals Inc.—also announced Monday—representing a premium of 255%.

The outcome of the Hillshire sale highlights the risks, and potentially rich rewards, of takeover auctions. Not all company sales happen via auctions. Often, buyers prefer to negotiate with a target one-on-one, and leave the possibility of a so-called topping offer for after the signing of a deal. Buyers typically prefer this approach; they see auctions as opaque and leaving them at risk of overpaying.

Sometimes in an auction, “the winner is the loser,” said one deal maker.

As for sellers, even in sales processes where there isn’t much interest from buyers, advisers try to create the appearance of demand using tricks like telling an interested party that his company’s meeting has a hard stop at a certain time, the implication being that another bidder is arriving, said one deal maker.

“Clearly when we are advising on the sell side we use both the actual competition and the illusion of competition to our advantage,” said Samuel Waxman, an M&A partner at Shearman & Sterling LLP uninvolved in this auction.

In Hillshire’s case, the company’s bankers at boutique Centerview Partners and Goldman Sachs Group Inc. organized a rapid-fire auction that set them up to quickly extract the best-possible bid with minimal leaks, after Tyson and Pilgrim’s Pride both made unsolicited offers that were announced or confirmed.

Pilgrim’s Pride first offered $45 per share on May 27, followed by a $50 per share offer from Tyson on May 29 and then a higher, $55-a-share offer from Pilgrim’s Pride last week.

The auction was a three-tiered event with the potential for pressure to mount along the way. Each side was to submit a first-round bid by Sunday at 4 p.m., according to people familiar with the matter. If one bid bested the other by $2.50 per share, that bid would win, the people said. But if the bids came in within that amount, each company would have the chance to participate in a new round of bidding, said the people.

If bids in the second round came within $1.25 per share of each other, there would be another, final round of bids where Hillshire would go to the highest bidder, the people said.

In the first round, Pilgrim’s Pride, represented by Lazard, didn’t raise its offer from $55 per share, said the people. Tyson, in an effort not to take any chances at missing out, according to one person familiar with the matter, submitted a $63 per share offer. Had Tyson, advised by Morgan Stanley and J.P. Morgan Chase & Co., submitted an offer of around $57.50 per share, it would have won the auction, the people said.

At $63 per share, Tyson, based in Springdale, Ark., is paying a multiple of 16.7 times Hillshire’s adjusted earnings before interest, taxes, depreciation, and amortization over the past year, which some bankers say is high for consumer deals.

Tyson’s Mr. Smith on Monday said the price is well worth it. “Brands like Hillshire [lunch meat] and Jimmy Dean and Ball Park [hot dogs], they don’t become available very often.”

Both Tyson and Pilgrim’s sought to outdo Hillshire’s own planned purchase of Pinnacle Foods Inc., PF -1.00% maker of Vlasic pickles and Wish-Bone salad dressing, for $4.3 billion. Hillshire is expected to scuttle that deal so it can consummate the Tyson transaction, which is a condition of Tyson’s offer. Hillshire said Monday that its board hasn’t yet approved the deal with Tyson and hasn’t changed its recommendation regarding the Pinnacle merger.

One less-tangible benefit of the deal to Tyson: containing JBS. The Brazilian brothers who run the Sao Paulo-based firm, Wesley and Joesley Batista, used a spree of deals to transform JBS into what they say is the world’s largest meat company, and a chief rival to Tyson as both companies compete to serve growing global markets for meat.

The Batista brothers have long coveted Hillshire and its brands, but may now have to consider smaller, less-significant targets in the U.S.

Date: June 9, 2014