Healthcare Data Analytics and the Coming Revolution: How ready is the sector?

Healthcare Data Analytics and the Coming Revolution: How ready is the sector?

Recent reports have estimated the market size of healthcare analytics to be $ 10 Bn by 2018. This is a big market, and my guess is that the actual market size is much bigger. It all depends on what you count and how you count it.

Data, data, everywhere, but not enough insight to think

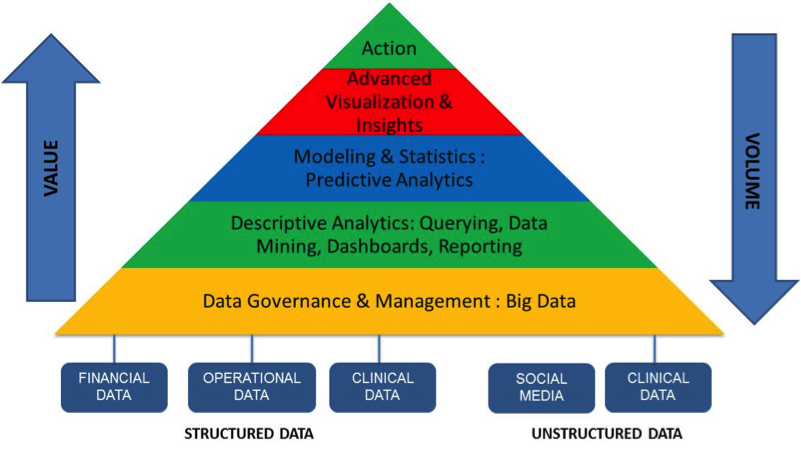

The framework below can be used to delineate the different aspects of analytics in the context of healthcare.

Want to publish your own articles on DistilINFO Publications?

Send us an email, we will get in touch with you.

There is a huge amount of data available in healthcare. This includes the following:

– Structured data (internal) : EMR systems, claims systems, revenue cycle systems

– Unstructured data (internal) : doctor notes, images

– Structured data (external): Public data ( CMS), benchmark data, syndicated data

– Unstructured data (external) : social media

This is obviously not an exhaustive set of data sources, which are ever-increasing as healthcare gets “democratized” and patients start taking control of their own medical and healthcare information. The emergence of new healthcare entities like ACO’s and HIE’s will make new data available as new products and care delivery models start pulling in previously underinsured and uninsured members of the population into the healthcare system. As a part of this, previously ignored data sources such as demographic data and individual credit histories will become important aspects of analyzing patient profiles. And as we go deeper into internal environments, healthcare companies will start looking at machine data to understand patient and provider behavior.

As medical devices become more remote and more connected, and patients start using mobile applications widely for a range of activities from self-diagnosis to shopping and paying for healthcare, and as remote patient monitoring devices become more common, the complexities of data sources (volume, velocity, variety) will multiply. This will create new challenges for health insurance companies to manage member engagement, and will make it very hard for primary care physicians to provide care unless based on the limited information and insights they have about patients from their internal systems alone.

The framework above indicates where the value and the volumes are. Traditionally, healthcare has focused on the “volume” end of analytics, namely data management and governance, and some degree of descriptive analytics. Very little, if anything is happening in the area of advanced analytics and predictive modeling. This is in sharp contrast to other sectors like retail and banking, which I will talk about later in this paper.

All this is not optional any more. In my conversations with senior healthcare executives, I get a sense that they recognize the situation but are understaffed for even their most basic reporting and analytical needs. Take, for example, the ACO marketplace. Meeting the needs of compliance reporting on 33 core quality measures alone requires these entities to invest in and establish a reporting infrastructure – and this is just to do business with CMS! Table stakes, in other words. What about all the other management information and dashboards that they need to manage their businesses successfully and qualify for the shared savings?

A new way of approaching the relationships between the 3 P’s (patient, provider, payer)

The traditional parts of healthcare, namely the payers and the providers, have been used to doing business on a fee-for-service model all these years, and all their information systems are set up to operate in this paradigm. The nature of the relationship was largely adversarial, with the focus being claims and payments, and a constant analysis of care delivery utilization for the purpose of contract negotiations between provider and payer. The new thinking on this focuses on collaboration for improved outcomes, while keeping costs low.

As population health, bundled payments and VBP go mainstream, a solid analytical foundation becomes essential to track and manage clinical and financial outcomes.

Take the case of penalties on preventable readmissions. Many hospitals across the nation have been penalized up to 1% of their Medicare reimbursements for failing to comply with readmissions thresholds. Hospitals are scrambling to understand the root causes of readmissions, and prevent or minimize these from occurring. Hospital executives are concerned not just with the bottom line impact but the reputational damage that accompanies being on a list of offenders. Payers, on the other hand, are looking at their member populations and their provider networks at a macro level to identify patterns that will help them address the readmissions problem at a cohort level that goes beyond clinical analysis at an individual patient level. New tools and risk-scoring models are required to tackle this problem effectively.

A big question that I get asked all the time is: what is the analytical maturity level of the healthcare system? The answer is a) it varies and b) it is relative to other sectors.

To take the first part, the healthcare system has developed fairly mature analytical capabilities in the traditional areas of focus like claims analysis, however that is mostly in the form of historical analysis for provider contracting (payers), or for claim denial analysis and improved recoveries (provider). The payer sector has developed fairly advanced systems for actuarial analysis in the traditional employer-based health insurance model; however they are in very early stages of understanding how to work in a marketplace that is shifting towards individual members. Internal data alone will no longer cut it, and the risk-management models of employer-based insurance will no longer suffice.

To address the second part, sectors like retail and banking do a great job of analyzing and anticipating “where the puck will be” and are prepared with messages and offerings for their consumers on a near real-time basis. Not that healthcare is awash with coupons yet (“Dear Customer, here’s a discount coupon for teeth whitening along with your root canal”), but then, the future is closer than we think.

OK, so I hire 50 data scientists and I’m covered?

Providers have spent huge sums of money implementing EMR systems and demonstrating meaningful use, to qualify for incentives. Now comes the question: what to do with the data? Clinical analytics and informatics has never been a focus in the fee-for-service model, so it’s a major change of mindset that’s required.

Everyone agrees that there is a huge need for analytics, and also that the capacity and capabilities required to meet those needs doesn’t exist today within the healthcare system. This cannot be addressed by launching an aggressive hiring program for data scientists – there just aren’t enough data scientists out there to go around (and who wants to work in healthcare when they could be out there working for Google or Amazon, or launching their own start-ups?). Nor can this be addressed by throwing the next new piece of technology that comes along at the problem.

The solution lies in prioritizing the areas of focus, developing a multi-year roadmap, and determining which areas are core to the business and which ones can be delivered using a combination of technology and consulting support. It’s also worthwhile considering global talent, especially from places like India where there is strong talent with backgrounds in science and applied math to take on at least some of the “heavy-lifting” aspects of an analytics program so that scarce and valuable internal resources can be focused on the domain-intensive aspects of analytical work.

It’s time for the healthcare sector to make bold, disruptive moves and embrace analytics whole-heartedly as a strategic tool for growth and profitability.

—————————————————————————————————

Paddy Padmanabhan is Sr VP of Healthcare Analytics for Symphony Teleca. He can be reached at paddy.padmanabhan@symphonyteleca.com.