In the past few years, expenditure incurred on healthcare has been on the rise, encompassing expenses on preventive check-ups, medical insurance, etc. Income-tax Act, 1961 (the Act) provides certain tax deductions for an individual in respect of such expenditure incurred on self or dependents, which have been discussed in this article.

Mediclaim/Health insurance premium

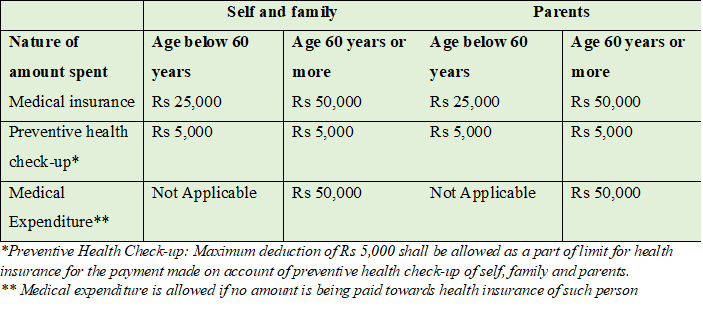

For individuals, deduction is allowed for premium paid under a medical insurance policy covering his/her own health or his/her family’s (i.e., spouse and dependent children) up to Rs 25,000 per annum. Further, an individual can claim a deduction for the premium paid under a medical insurance policy covering his/her parent or parents up to Rs 25,000 per annum. In case the said individual, spouse or parents are resident senior citizens (i.e., of the age 60 years or more), then the aforesaid deduction limit is enhanced to Rs 50,000 per annum. Expenditure incurred on preventive health check-up of up to Rs 5,000 per annum for self and family and/or parents, respectively can also be claimed as a deduction. This deduction is irrespective of the individual’s age and within the overall limits mentioned above.

In the case of a salaried individual, it is possible that medical insurance coverage is provided by the employer (either by way of direct payment under a medical insurance policy with the insurance company for the employee or reimbursement of such premium to the employee for the coverage of the employee and his/her family). Such premiums paid/reimbursed by the employer are tax-free perquisites for the employee. The employee may also opt for a higher coverage, upon being given a choice by the employer, by paying a top-up premium at his/her own expense. Such premium would be eligible for a deduction under Section 80D of the Act. The employer can consider such a deduction while deducting tax at source (TDS) on taxable salary.

All of the above deductions referred in the above two paragraphs can be allowed by the employer at the time of computing TDS on taxable income if the employee furnishes the requisite receipts/documents. Alternatively, the employee can claim the same at the time of filing income-tax return for that particular Financial Year (FY).

Medical expenditure

Want to publish your own articles on DistilINFO Publications?

Send us an email, we will get in touch with you.

A resident senior citizen, who is not covered under any mediclaim insurance scheme, can claim a deduction for actual medical expenditure incurred during a particular FY. Deduction can be claimed up to Rs 50,000 for the expenditure incurred on own or family’s health and an additional Rs 50,000 on parents’ health. No documents have been prescribed under the Act to be maintained for claiming this deduction; however, it would be prudent to maintain a record of prescription, along with copy of diagnostic tests, medicine bills, invoice copy for treatment etc. It is pertinent to note that this deduction can only be availed when no amount is being paid towards the health insurance of such individual.

Mode of payment for the purpose of eligible deduction under this Section should be other than cash, except for expenses incurred towards preventive health check-ups for self and family and/or parents.

Deduction limits under different scenarios are summarised as under:

Treatment for disability/severe disability

Besides the above, a deduction of Rs 75,000 per annum is allowed to a resident individual under Section 80U of the Act who is suffering from specified disability as certified by a specified medical authority. In case such an individual suffers from any specified severe disability, the deduction limit is enhanced to Rs 1,25,000.

For a resident individual, who has incurred an expenditure in respect of maintenance, including medical treatment of a dependent who is suffering from a specified disability or specified severe disability, a deduction is allowed under Section 80DD of the Act of Rs 75,000 and Rs 1,25,000, respectively. This deduction is allowed provided no deduction has been claimed under Section 80U of the Act as mentioned above.

Deduction for prescribed diseases and ailments

Expenditure incurred by a resident individual on medical treatment of certain prescribed diseases or ailments (such as neurological diseases and malignant cancers) of self or dependents are eligible to claim deduction up to Rs 40,000 under Section 80DDB of the Act. However, in case the dependent is a senior citizen, the amount of deduction is available up to Rs 1,00,000.

Dependents for the purpose of the aforesaid deductions (i.e. Section 80DD and 80DDB of the Act) include spouse, children, parents, brothers and sisters, who are wholly or mainly dependent on such individual for support and maintenance. The individual claiming such deductions shall obtain a copy of the certificate issued by the prescribed medical authority in the specified form and manner, in respect of the relevant FY.

With ever-rising cost of medical treatment, it is worthwhile for individuals to be aware of the potential tax deduction for the medical insurance/expenditure that they are incurring.

Source: Money Control